Venmo Walked, So Tokenized Deposits Could Run

And USDC Ran to the Markets

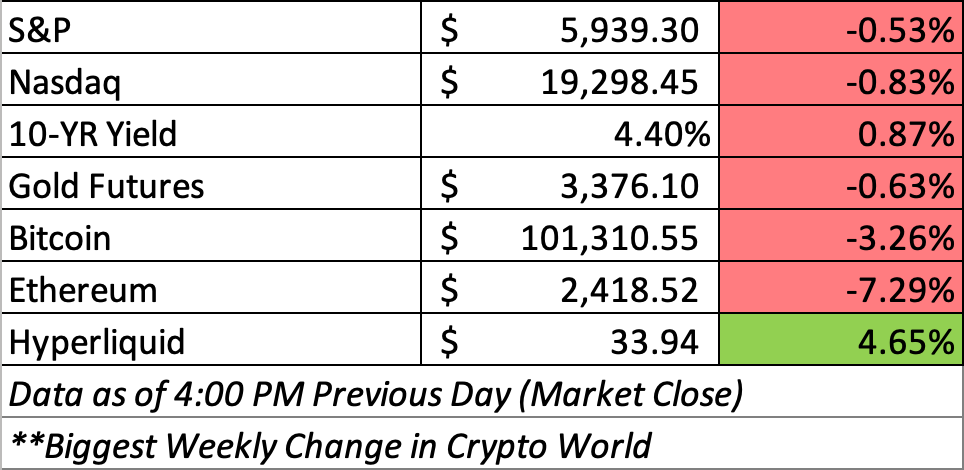

Good Morning & Happy Friday! The S&P 500 fell 0.53% on Thursday, led by a sharp 14% drop in Tesla shares, which caused the company to lose its trillion-dollar market cap. The decline followed a public feud between Donald Trump and Elon Musk, with Trump expressing disappointment in Musk and threatening to cut off government contracts. Musk responded defiantly, claiming Trump would have lost the election without him.

Markets were also rattled by news of a phone call between Trump and Chinese President Xi Jinping. While Trump described it as a "very good" call, no concrete outcomes were announced. Although U.S.-China tariffs were temporarily eased in May—boosting markets—investors remain wary of renewed tensions. Analysts remain skeptical about a quick trade resolution.

Circle’s IPO officially happened yesterday and the company surged above its IPO price. Read more on that below. And from PayPal to Venmo to China's superapps, the digital payments revolution is now entering a new era as HSBC launches tokenized deposits. Lastly, be sure to check in on the latest moves in the BIR portfolio.

Crypto IPO Alert: Circle IPO

Shares of Circle Internet Group, a stablecoin company, surged 168% on its first trading day after raising nearly $1.1 billion in an IPO. The stock opened at $69, well above its IPO price of $31, and peaked at $103.75, valuing the firm at around $6.8 billion.

This is Circle’s second attempt to go public after a failed SPAC merger in 2022. CEO Jeremy Allaire emphasized the importance of regulation and government partnerships, highlighting Circle’s role as one of the most licensed and transparent firms in crypto.

Founded in 2013 and based in New York, Circle is best known for its USDC stablecoin, developed with Coinbase, which remains a minority stakeholder. USDC is the second-largest stablecoin, trailing only Tether (USDT).

The IPO comes as the crypto industry experiences a favorable U.S. political climate, with stablecoins attracting growing interest from banks and corporations due to their potential for faster, cheaper payments. Analysts predict the stablecoin market could grow 10-fold, creating a trillion-dollar opportunity.

From PayPal to Tokenized Dollars: How the Future of Payments Is Being Built by Global Banks

For most Americans, the journey to digital payments began with PayPal. Launched in the early 2000s, PayPal transformed how people paid for things online. It made it easy to send money with just an email address—no need to write checks or share bank details. It was a major breakthrough, but it still sat squarely on top of the traditional banking infrastructure. Payments could take a day or two to clear, and the backend remained tethered to legacy systems like ACH and credit card networks.

Venmo, acquired by PayPal in 2013, took things a step further. It was the first app to make peer, to, peer payments feel truly social and instantaneous. Sending $20 to split a pizza or pay your roommate became as easy as texting. The transaction speeds were still ultimately dependent on banking rails, but the experience was faster, friendlier, and designed around real, time mobile interactions. Venmo became a verb, and millions of younger Americans adopted it as their primary money movement tool.

While this was playing out in the U.S., something even more radical was happening in China. Ant Financial, now Ant Group, built Alipay into a full, blown financial ecosystem. Originally a payments solution for Alibaba’s online marketplace, Alipay evolved into a ‘superapp’. Users could store money, pay bills, invest, take out loans, and even buy insurance, all from one interface. Ant didn’t just layer on top of banks, it replaced many of the functions banks traditionally performed. By 2020, Alipay served over a billion users and processed trillions in payments, reshaping consumer finance in China and creating a model the rest of the world would come to study.

Now, in 2025, the next phase of payment innovation is arriving, not from a fintech startup or a social app, but from one of the world’s most established banks. HSBC, a global financial institution with deep roots in Asia, Europe, and North America, has launched tokenized deposits in Hong Kong. Unlike PayPal or Venmo, which simply improve the interface of existing systems, HSBC is changing the infrastructure itself.

Tokenized deposits allow companies to convert U.S. dollars or Hong Kong dollars held in an HSBC bank account into blockchain, based tokens that can be used for instant, 24/7 payments. These are not stablecoins like USDC or Tether, which are issued by private firms and backed by reserves held elsewhere. These are digital representations of real deposits, created and guaranteed by a licensed bank. The settlement is final and happens in seconds, not hours or days.

What makes HSBC’s launch truly noteworthy is the introduction of instant U.S. dollar settlement on, chain by a global bank. For companies operating internationally, especially those based in Asia, being able to settle in USD instantly, around the clock, without depending on correspondent banking networks or time, zone constraints, is a game changer. It drastically reduces transaction costs, improves cash management, and brings much, needed efficiency to treasury operations.

The service has already been used by Ant International, the global payments arm of Ant Group, to transfer funds through its blockchain, based treasury platform. Backed by support from the Hong Kong Monetary Authority, this isn’t just a proof of concept, it’s a real financial product in a regulated environment.

HSBC’s move is part of a broader shift in global finance. More banks are exploring tokenization not just for payments, but for bonds, securities, and even gold. The goal is to create programmable money and financial assets that can move and settle in real time, with full regulatory compliance. Tokenized deposits bridge the gap between traditional banking and the decentralized potential of blockchain.

From the early days of PayPal and the mobile, first explosion of Venmo to the integrated financial ecosystems like Ant, we are now entering an era where money itself is becoming digital at the foundational level. Tokenized deposits may not feel as user, friendly as Venmo, yet, but they represent a much more significant change. For the first time, the same banks that hold your checking account are beginning to issue digital dollars that can move globally in seconds.

This is not just the future of payments. It’s the beginning of a new digital financial system, built not on the rails of the past, but on the networks of tomorrow.

Keep reading with a 7-day free trial

Subscribe to The Blockchain Income Report to keep reading this post and get 7 days of free access to the full post archives.