The Great Tokenization Shift

And how much is Aave making?

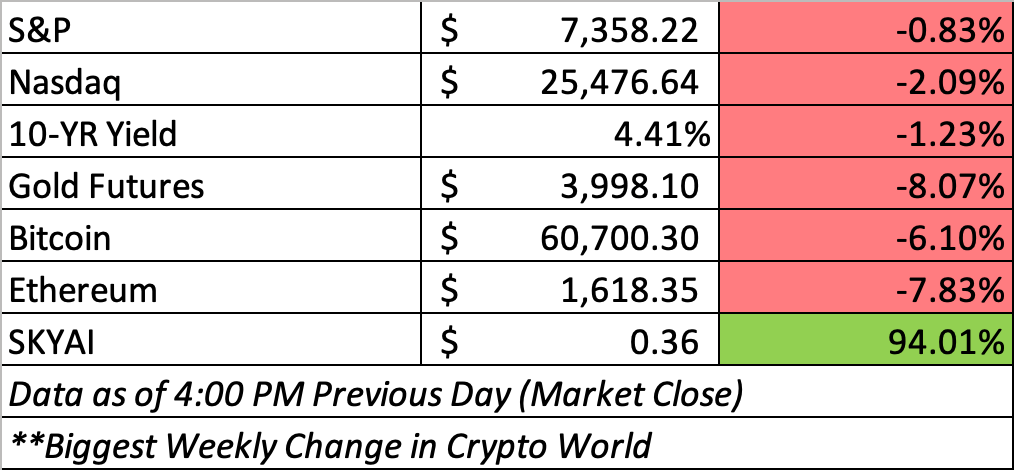

Good Morning. U.S. stocks struggled to recover from a sharp tech-led selloff, with the tech-heavy Nasdaq Composite and S&P 500 finishing lower as investors continued taking profits in high-flying AI stocks.

Concerns over stretched valuations, heavy AI-related spending, and the potential for higher interest rates weighed on the sector, while the more industrial-focused Dow Jones Industrial Average managed a modest gain. At the same time, oil prices fell sharply to their lowest levels since the start of the U.S.-Iran conflict as tanker traffic resumed through the Strait of Hormuz, easing some concerns about supply disruptions.

Crypto markets were volatile over the past week, with both Bitcoin and Ethereum finishing lower as risk appetite weakened and traders reacted to broader macro uncertainty and choppy trading conditions.

This week we discuss how tokenization is evolving from a crypto-native concept into a core priority for major financial institutions building the next generation of market infrastructure.

Tokenization Is Becoming an Exchange Issue

For much of the last decade, tokenization was treated as a crypto story. It was discussed in the language of decentralized finance, stablecoins, real world assets and experiments at the edge of the financial system. The basic idea was simple enough: take an asset that exists in the traditional world and represent it digitally on a blockchain. That asset could be a Treasury bill, a share of stock, a private fund interest, a deposit, a commodity claim or even a piece of real estate.

What is changing now is not only the technology, but the identity of the institutions paying attention. Tokenization is no longer just a project for crypto startups. It is increasingly becoming a strategic concern for the world’s major exchanges, clearing houses and market infrastructure providers.

The recent joint venture between OKX and Intercontinental Exchange, the owner of the New York Stock Exchange, is an important example of this shift. The venture is expected to operate as a regulated U.S. broker dealer and futures commission merchant, allowing OKX customers to access ICE futures and potentially NYSE tokenized equities markets. Former New York Governor Andrew Cuomo is serving as co chair, underscoring the political and regulatory dimension of the project.

The symbolism matters. ICE is not a speculative crypto firm looking for attention. It owns some of the most important financial infrastructure in the world, including the NYSE. Its involvement suggests that tokenization is being taken seriously not as a replacement for regulated markets, but as a possible upgrade to them.

The attraction is easy to understand. Traditional securities markets still operate within a structure built around business hours, delayed settlement, fragmented custody and multiple layers of intermediaries. That system is highly reliable, but it is also expensive and slow. Tokenization offers the possibility of markets that trade continuously, settle faster, support fractional ownership and allow collateral or cash to move more efficiently across platforms.

This is particularly important for global investors. U.S. equities are among the most widely demanded assets in the world, but access remains uneven. Investors outside the United States often face frictions related to brokerage access, local custody, market hours and settlement. A properly regulated tokenized equity market could allow investors to gain exposure to the same underlying economic assets in a more flexible digital format. That does not mean investor protections disappear. In fact, the most important tokenization projects are moving in the opposite direction: they are trying to combine blockchain efficiency with existing legal and regulatory safeguards.

This is why exchanges are paying attention. Exchanges are not simply venues where buyers and sellers meet. They are trust engines. They provide rules, listings, surveillance, clearing relationships, data, liquidity and credibility. If tokenized assets become a major financial product, the institutions that already control trusted market infrastructure will not want to watch from the sidelines.

The same logic applies beyond equities. CME Group has been working on tokenized cash and settlement tools that could allow institutional clients to move value continuously for margin, collateral and settlement workflows. This points to one of the most practical uses of blockchain technology: not replacing markets, but reducing friction inside them. In derivatives markets, where collateral must be posted, moved and optimized constantly, faster settlement and more mobile collateral could have real economic value.

DTCC is also moving in this direction through its tokenization initiatives. This is significant because DTCC sits at the heart of U.S. post trade infrastructure. If the exchange represents the front end of the market, DTCC represents much of the back end. Tokenization only becomes truly powerful when both sides evolve: the trading venue and the settlement infrastructure.

The important point is that tokenization is no longer a single product category. It is becoming a design principle for financial markets. Tokenized equities address access and trading hours. Tokenized deposits address payments and treasury management. Tokenized Treasuries address collateral and yield. Tokenized fund interests address private market access. Each use case is different, but the common theme is the same: financial assets are being rebuilt so they can move more like software.

There are still substantial challenges. Regulators must decide how tokenized claims map to traditional legal ownership. Exchanges must ensure that tokenized markets do not fragment liquidity or create weaker investor protections. Issuers must prove that token holders have enforceable rights. Custodians must show that assets are properly backed. And investors must understand the difference between owning a token that references an asset and owning the asset itself.

These issues are not minor. In fact, they explain why the involvement of major exchanges matters so much. Crypto native firms brought the innovation. Traditional market operators bring the legal structure, institutional relationships and operational discipline needed for mass adoption.

The next phase of tokenization will probably not look like the early crypto boom. It will be more regulated, more institutional and less ideological. It may also be far more consequential. If exchanges, banks, clearing houses and asset managers begin using blockchain rails for securities, deposits and collateral, tokenization will move from a niche investment theme to a core part of global financial infrastructure.

For investors, this creates an important opportunity and a warning. The opportunity is that tokenization could reshape how assets are issued, traded and settled. The warning is that not every tokenization project will benefit equally. The winners are likely to be the platforms that combine regulatory credibility, deep liquidity, technical execution and real market demand.

Crypto News You Can’t Miss: Brazil Brings DeFi Into the Tax Net

Brazil has introduced stricter crypto reporting requirements through Normative Instruction No. 2,291/2025, significantly expanding tax transparency and oversight of digital asset transactions. Under the new rules, individuals and businesses must report crypto activity conducted through foreign exchanges, decentralized finance (DeFi) platforms, or direct peer-to-peer transactions when monthly transaction volumes exceed BRL 35,000. The framework broadens the range of reportable activities to include purchases, sales, staking, airdrops, and crypto-to-crypto trades, with filings submitted electronically through Brazil’s tax portal. Failure to comply can result in monthly fines, making accurate record-keeping and reporting increasingly important for crypto users and businesses operating in the country.

For crypto users in Brazil, the changes mean greater accountability and a reduced ability to operate outside the view of tax authorities, particularly when using foreign platforms or DeFi protocols. While the new requirements create additional compliance obligations, they also provide clearer regulatory guidance and reduce uncertainty around how crypto activities should be treated for tax purposes.

More broadly, the regulation reflects a global shift toward integrating crypto into existing financial and tax systems rather than treating it as a separate or lightly regulated market. By aligning with international standards such as the Crypto-Asset Reporting Framework (CARF), Brazil is increasing transparency, improving regulators’ visibility into cross-border crypto activity, and strengthening efforts to combat money laundering and illicit finance. Although this may reduce some of the anonymity historically associated with crypto, it also represents another step toward mainstream adoption, helping legitimize the industry and creating a clearer regulatory environment that could encourage greater institutional participation and long-term growth of the digital asset economy.

Media of the Week: Aave’s Revenue Generation

Aave is a decentralized lending marketplace where users supply capital, borrowers take loans, and the protocol earns fees for facilitating those transactions. Revenue has reached record highs and is continuing to grow in 2026, even before several anticipated product upgrades are released, leading many investors to expect further growth ahead.

What's especially notable is that Aave generates this revenue with:

no physical branches,

no loan officers,

no large sales force,

and a relatively small team.

Its all about efficiency,