The Chain Reaction

And The Stablecoin Civil War

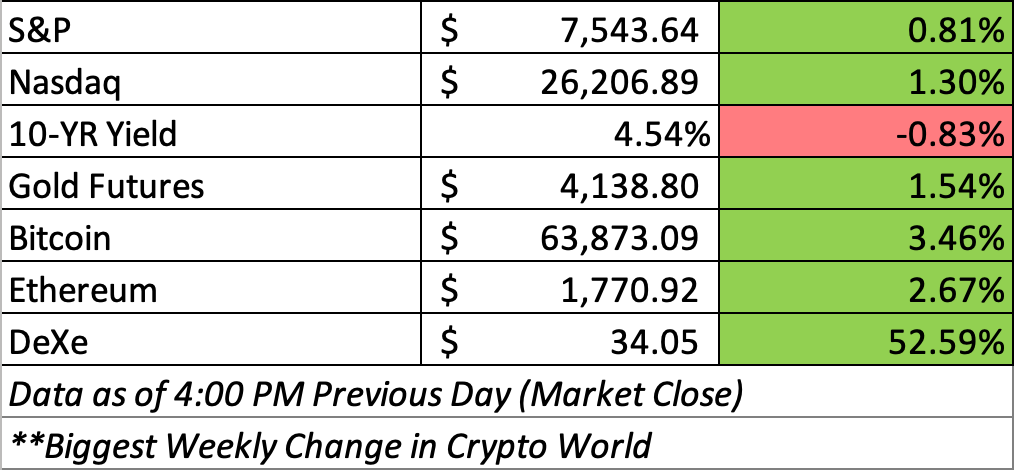

Good Morning & Happy Friday! U.S. stocks moved higher on Thursday, led by a rally in semiconductor shares and lower oil prices, as investors looked past renewed U.S.-Iran tensions.

Although the U.S. launched another round of strikes on Iran following attacks on commercial shipping in the Strait of Hormuz, oil prices declined after President Donald Trump said Iran had reached out to negotiate. Despite the market’s resilience, analysts cautioned that geopolitical uncertainty and persistent inflation risks could keep markets volatile.

Over the past 24 hours, crypto markets traded cautiously as geopolitical tensions in the Middle East kept Bitcoin and Ethereum largely rangebound, while Arbitrum (ARB) outperformed on strong adoption of Robinhood’s new Layer-2 blockchain, helping lift the broader crypto market modestly.

From Arbitrum's Robinhood-powered breakout to the emerging battle over open stablecoin infrastructure, we examine two stories that could reshape crypto's next phase. And don’t forget to check out the BIR portfolio!

Crypto News You Can’t Miss: Robinhood Launches New Chain

Arbitrum’s ARB token surged 19% after strong early activity on Robinhood’s new blockchain, Robinhood Chain, which is built using Arbitrum’s technology. The network generated more than $568 million in trading volume on Wednesday and another $350 million on Thursday, driven largely by memecoin trading, while stablecoin deposits exceeded $260 million in its first week. Under Arbitrum’s Expansion Program, 10% of the net revenue from chains built on its technology flows back to the Arbitrum ecosystem, giving it a direct financial benefit from Robinhood Chain’s growth. The Arbitrum Foundation estimates the chain is already on pace to generate more than $12.5 million in annualized revenue, with additional upside expected as tokenized real-world assets gain traction.

Robinhood launched the blockchain alongside broader crypto initiatives, including tokenized U.S. stocks, DeFi-powered savings, and AI-driven trading tools. While the initial surge in trading activity may moderate, ARB’s price rally suggests investors view Robinhood Chain as a meaningful long-term revenue driver for the Arbitrum ecosystem rather than simply another distribution partnership.

The Stablecoin War Will Not Be Won by a Stablecoin Company

, a new stablecoin backed by more than 140 financial and crypto firms, including Visa, Mastercard, Stripe, BlackRock and Coinbase. The goal is to make")

The stablecoin race is usually described as a battle between issuers. Tether versus Circle. USDT versus USDC. Offshore dominance versus regulated legitimacy. The story is familiar, simple and very possibly wrong.

Our view at the BIR is that the stablecoin war may not be won by a stablecoin issuer at all. It may be won by the companies that decide stablecoins are too important to be controlled by any one company.

This week we are looking at a new startup called the Open Standard. Open Standard, the independent company announced on June 30, 2026, is launching Open USD, or OUSD. It is being led by Zach Abrams, the co-founder of Bridge, the stablecoin infrastructure company acquired by Stripe. The company is not positioning OUSD as simply another dollar stablecoin trying to compete for market share. It is positioning it as neutral infrastructure for payments, trading, treasury and internet commerce. That may sound like a subtle distinction, but we think it is the whole point.

Stablecoins have spent years being treated as products. USDT is a product. USDC is a product. PYUSD is a product. Each has a brand, an issuer, a balance sheet, a regulatory profile and a business model. Open Standard is trying to make a different argument. It is saying that the market does not need another proprietary dollar token. It needs a common standard that many companies can use, distribute and build around.

The reported backer list makes this more than a crypto story. Open Standard has brought together more than 140 companies, including Visa, Mastercard, American Express, Stripe, BlackRock, Coinbase, Google, BNY, Standard Chartered, Ripple and Shopify. These companies are not natural allies. Visa and Mastercard compete every day. Stripe competes with payment processors, banks and fintech platforms. Coinbase and Ripple have very different visions for crypto infrastructure. BlackRock and BNY sit deep inside the traditional financial system.

So when companies like this gather around the same stablecoin project, it is worth paying attention. They are not doing it because they suddenly agree on everything. They are doing it because a shared stablecoin standard may be more useful than a world where every major platform issues its own dollar token.

The economics are especially important. OUSD is expected to allow businesses to mint and redeem without fees and without volume limits. Instead of allowing one issuer to capture most of the reserve income, Open Standard plans to share much of that income with the partners that distribute and integrate the stablecoin, after operational costs. Governance is also meant to be collective, with Open Standard operating as an independent entity rather than as a token controlled by one exchange, bank, payment network or technology company. That structure goes directly at the heart of the stablecoin business model.

For years, the assumption has been that issuance is the prize. If you issue the stablecoin, you capture the reserve income. If you capture the reserve income, you build a powerful financial business. If your token becomes widely used, you become part of the payment infrastructure.

But we think that framing misses something important. Stablecoins are only valuable because other people use them. The value comes from distribution, liquidity, payment volume, merchant acceptance, wallet integration, exchange activity and trust. In other words, the value is often created by the platforms, fintechs, exchanges, wallets, banks and merchants that bring the users. From that perspective, the issuer should not be the king. The issuer should be the plumbing.

This is where Circle’s position becomes more complicated. USDC is the leading regulated dollar stablecoin, and Circle deserves enormous credit for building it. But success creates its own tension. As Circle expands into payment networks, dedicated blockchain infrastructure and broader financial services, some partners may start to ask a reasonable question: is Circle enabling us, or is Circle gradually becoming a competitor?

That is what makes Open Standard potentially provocative. It offers a different bargain. Instead of one issuer controlling the token, the rails and the economics, it proposes a shared model where the companies that drive adoption also participate in the upside.

We do not think this guarantees success. Announcing a consortium is the easy part. Making it work is much harder. The history of payments is full of alliances that looked impressive on paper and then became trapped in governance, incentives and politics. Getting banks, payment networks, fintechs, crypto firms and technology companies to agree on rules will not be simple. They will need to agree on reserve management, redemption rights, compliance standards, chain support, revenue sharing and control. That is a serious challenge. But it is also the challenge that matters.

The better historical analogy here is not Bitcoin. It is Visa. Visa became powerful because banks needed a shared acceptance network. They could cooperate on the standard while still competing for customers. That structure was messy, but it worked. Dee Hock described Visa as a “chaordic” organization, part chaos and part order. Stablecoins may need something similar: enough coordination to create trust, but enough openness to prevent any one company from capturing the entire system.

Libra tried to move in this direction before. It failed because the political environment was hostile and because Facebook was the wrong sponsor for a global money project. But the underlying idea was not foolish. A global digital money standard becomes more powerful when wallets, merchants, exchanges and platforms can build on top of it.

The difference now is that the world has changed. Stablecoins are no longer theoretical. Banks are experimenting with tokenized deposits. Payment companies are building blockchain settlement tools. Asset managers are moving funds onchain. Regulators are not simply asking whether stablecoins should exist. They are asking how stablecoins should be regulated.

Our view is that the stablecoin market does not need hundreds of isolated dollar tokens. It does not need every bank, fintech, exchange and payment company launching its own version of digital cash. That path leads to fragmentation, liquidity silos and unnecessary complexity. It also makes the user experience worse, because money becomes less useful when it has to be constantly converted, bridged or redeemed.

The more interesting future is one where companies compete above the stablecoin layer, not for ownership of the stablecoin layer itself. Exchanges can compete on trading. Wallets can compete on user experience. Payment companies can compete on merchant acceptance. Banks can compete on custody, compliance and treasury services. But the base unit of digital dollars could become more standardized.

If Open Standard succeeds, it will not just challenge Tether or Circle. It will challenge the idea that the most important stablecoin business is issuing the stablecoin.

That is the provocative point. The winning stablecoin may not be the one with the loudest brand, the biggest issuer or the strongest first-mover advantage. It may be the one that becomes boring enough, neutral enough and useful enough that everyone can build on it.

Keep reading with a 7-day free trial

Subscribe to The Blockchain Income Report to keep reading this post and get 7 days of free access to the full post archives.