Walmart Eyeing...Crypto?

If Walmart is on board, that means everyone is.

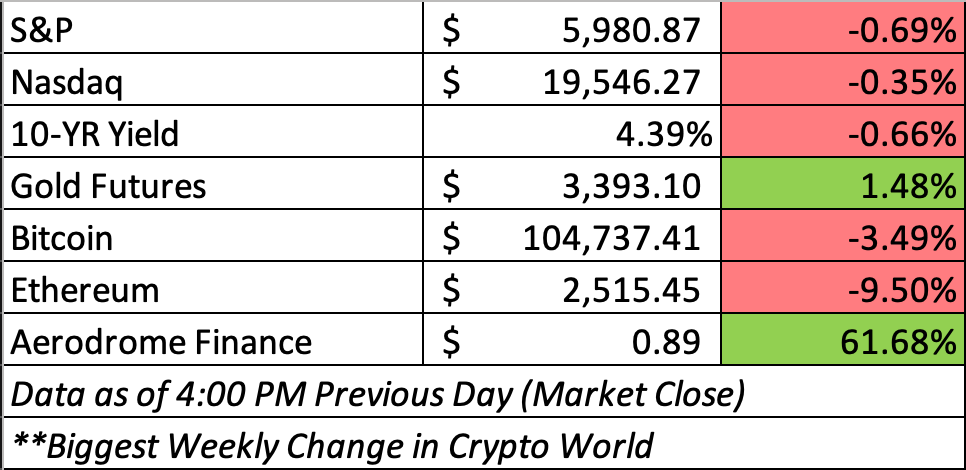

Good Morning! U.S. markets ended slightly mixed on Wednesday after the Federal Reserve held interest rates steady (4.25%–4.5%) and signaled it would “wait-and-see” to assess the impact of Trump-era tariffs on inflation before making changes.

Though the Fed projected two rate cuts later this year, it also lowered 2025 growth forecasts (to 1.4%) and raised core inflation estimates (to 3.1%), suggesting possible stagflation concerns. Geopolitical tensions added pressure, as the Israel-Iran conflict escalated into its sixth day.

Today, we cover the some of the more interesting crypto news from new fundraises, to the latest regulatory updates, and finally major blue-chip corporations like Walmart and Amazon eyeing stablecoins. Enjoy!

Crypto News You Can’t Miss: Senate Passes GENIUS Act

On Tuesday, the Senate passed the GENIUS Act, a landmark bill regulating U.S. dollar-pegged stablecoins, by a 68-30 vote. The legislation introduces federal oversight for stablecoins, requiring full reserves, monthly audits, and anti-money laundering compliance. It also allows banks, fintechs, and major retailers to issue regulated digital dollars.

The bill marks a major step forward for the crypto industry and it gives broad “authority to Treasury Secretary Scott Bessent, who believes the U.S. stablecoin market could surpass $2 trillion soon.”

Now headed to the House, the GENIUS Act must be reconciled with the House's STABLE Act, which differs in its regulatory structure. While both bills prohibit yield-bearing stablecoins, the Senate version centralizes oversight with the Treasury, while the House splits it among multiple agencies.

Despite initial hopes that regulating stablecoins would be easy, the bill faced months of negotiation and political friction. Nonetheless, it represents a turning point in the legitimization and regulation of crypto in the U.S.

In Walmart We Trust?

The recent news that Walmart and Amazon are exploring the use of stablecoins as payment solutions, coupled with Circle’s high-profile IPO, has sharpened the focus on the role of stablecoins in the United States economy. At first glance, the need for a stablecoin in a country with a mature, reliable, and technologically advanced payment system may not be immediately obvious. After all, the U.S. payment infrastructure enables billions of transactions each day with efficiency and security. Yet beneath this surface lies a key driver of corporate and small business interest in alternatives such as stablecoins: the high costs that businesses incur in the form of credit card transaction fees. These fees, quietly deducted from countless purchases, represent a persistent drain on margins for companies both large and small. It is against this backdrop that stablecoins are emerging as a potentially transformative tool in corporate America’s ongoing effort to reduce payment processing expenses.

For small businesses, credit card fees have long been a source of financial strain. Each time a customer swipes a credit card, the merchant typically pays an interchange fee that can range from 2% to 3% of the transaction value. Added to this are assessment fees, processing charges, and, for some businesses, gateway or service provider costs. While these fees may seem manageable on a per-transaction basis, their cumulative effect can be significant, particularly for small retailers, restaurants, and service providers operating on narrow profit margins. For many such businesses, credit card fees can be greater than their profit margin, that either diminish profitability or are passed on to consumers through higher prices.

Large corporations face a similar challenge, albeit on a vastly larger scale. Walmart, for instance, is believed to pay over $3 billion annually in credit card-related fees, with some estimates from earlier periods suggesting that the total could be even higher. Given Walmart’s enormous transaction volume and low-margin retail model, these fees represent a meaningful cost center. It is no surprise, then, that Walmart has long sought ways to reduce or bypass them. One of its most notable efforts came in the form of its pursuit of a banking charter. For nearly a decade, Walmart tried to establish an industrial loan company (ILC), arguing that it had no intention of operating a retail bank but simply wanted to process its own credit and debit transactions more cost-effectively. The proposal faced staunch opposition from lawmakers, community banks, and large financial institutions, all of whom feared the competitive disruption that might follow. Walmart ultimately withdrew its application in 2007, having concluded that the regulatory and political headwinds were too strong to overcome.

In the years since, Walmart has continued to expand its in-house financial services through partnerships and branded offerings, including check cashing, prepaid debit cards, and money transfers. However, the fundamental challenge of credit card fees has remained. This is where stablecoins enter the picture. Stablecoins, digital tokens pegged to the value of fiat currencies such as the U.S. dollar, are designed to provide the benefits of cryptocurrency (speed, transparency, programmability) without the volatility that characterizes assets like Bitcoin. By creating or accepting stablecoins, Walmart and other retailers could, in theory, establish internal payment ecosystems that sidestep traditional credit card networks entirely. Such a system could allow customers to load funds into a stablecoin wallet and transact directly with the retailer, avoiding the need for intermediaries like Visa or Mastercard.

The potential benefits to Walmart are clear. Eliminating or reducing credit card fees could save the company hundreds of millions of dollars annually. Moreover, a proprietary stablecoin could give Walmart greater control over its payments ecosystem, enabling faster settlement times, integration with loyalty programs, and the ability to offer targeted discounts or incentives for customers using the preferred payment method. Importantly, these innovations could also enhance data collection on consumer spending, a valuable asset in the age of data-driven retail.

The implications extend beyond Walmart. Should a major retailer successfully implement stablecoin payments, it could catalyze a broader shift among other large companies, each seeking similar cost savings and operational advantages. Indeed, if stablecoins prove effective at reducing payment processing costs, their adoption could accelerate across industries, challenging the longstanding dominance of credit card networks in consumer transactions.

Yet several hurdles remain. Regulatory clarity will be critical. While Congress is now considering legislation that would create a framework for private stablecoin issuance, the legal landscape remains in flux. Without clear guidelines, many companies may hesitate to make substantial investments in stablecoin infrastructure. Additionally, consumer adoption is not guaranteed. While tech-savvy customers may be quick to embrace stablecoins, the broader public may require time, education, and meaningful incentives to shift away from familiar card-based payments.

In sum, the emergence of stablecoins as a corporate payment tool reflects both longstanding frustrations with the costs imposed by existing payment systems and the promise of new technology to address them. Walmart’s exploration of stablecoins is not merely a novel experiment; it is part of a decades-long effort to reduce friction and cost in retail transactions. As regulatory frameworks evolve and corporate interest grows, stablecoins may yet prove to be the catalyst for a broader transformation of how payments are made in the U.S. economy.

Media of the Week: New Startup Raises 2.5

Crypto startup Nook, raised $2.5M from some major VC groups including Coinbase Ventures. The next tweet goes on to explain that the app partners with other crypto on chain applications such as Moonwell, Aave and Morpho to help non-defi-native users access yield opportunities on chain from their Coinbase wallet. Innovation like this is cool to see!