Finding Signals in the Golden Arches

From Big Mac Index to Snack Wraps

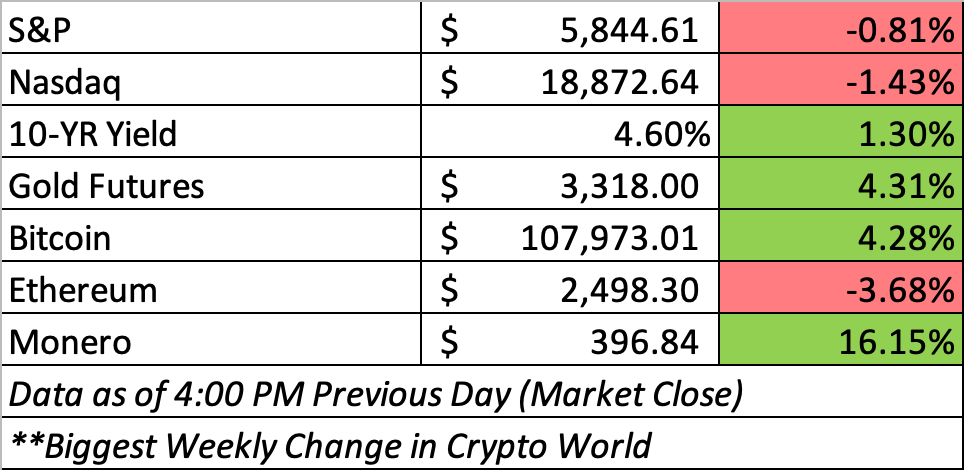

Good Morning. Stocks fell sharply on Wednesday as a surge in Treasury yields spooked investors, driven by concerns that a new U.S. budget bill could worsen the national deficit. Yields on long-term government bonds jumped, with the 30-year reaching 5.09%—its highest since October 2023—and the 10-year rising to 4.59%.

Today we cover a few topics ranging from new stablecoin legislation moving its way through Congress and the newest financial signals coming from McDonald’s. Lastly, despite a recent market rebound and growing optimism, the underlying economic risks suggest that the storm has not passed, and investors should remain cautious, with crypto and AI emerging as potential long-term hedges amid uncertainty. Read more on that below.

Crypto News You Can’t Miss: GENIUS ACT

The Senate has advanced the GENIUS Act, a major cryptocurrency regulation bill focused on stablecoins, with a bipartisan 66-32 vote. This comes two weeks after Senate Democrats initially blocked the bill, but support was secured following a bipartisan agreement on an amendment that addressed Democratic concerns. The amendment adds new consumer protection measures, places restrictions on tech companies issuing stablecoins, and extends ethics rules to certain government employees, temporarily applying to figures like Elon Musk and David Sacks. Although many Democrats remain wary—particularly about the Trump family’s crypto involvement—key Democratic senators agreed to move the bill forward.

Of course, there’s always some loud dissenters. Senator Elizabeth Warren criticized the legislation for failing to close loopholes that could enable corruption, while others like Senator Mark Warner argued that regulating blockchain technology is essential for the U.S. to maintain a leadership role. Having passed the Senate, the GENIUS Act faces an uncertain future in the House, where different legislation is being considered. Crypto advocates view the bill as a step toward improving the financial system, while critics continue to push for stronger restrictions, especially on political figures profiting from digital assets.

Enemy Sighted, Enemy Met – Realpolitik Returns to the Market

By Tom Grant

“Enemy sighted, enemy met, I'm addressing the realpolitik.

Look who bought the myth, by jingo, buy America.”

— R.E.M., “Exhuming McCarthy” (1987)

Just over one month ago, we wrote a piece on why the current economic situation might be different than past economic crises that led to a slow down or correction. A month later, equities are back in the positive for the year and there seems to be growing optimism that tariff’s will not create a recession. Has the storm passed? We do not think so. There are a number of moving parts in this equation including the crypto play which could be a big beneficiary of this.

Underneath the surface, we see a number of key indicators that are flashing caution. The global economy is reshuffling, and while headlines have turned upbeat, structural tensions remain. In fact, we think this might be one of those moments when the market’s calm should make investors nervous.

The concerns that we saw on Liberation Day were calmed by the administration’s decision to pause some of the most aggressive tariff proposals, and markets have responded with a sigh of relief but we think that the real pain has yet to be felt. We expect to see a shortage of goods followed by price hikes, which will be inflationary as well as concerning for the consumer.

Perhaps more damaging is the uncertainty. For businesses with global supply chains, constant policy shifts on tariffs mean that long-term capital investment becomes riskier and harder to plan. That doesn’t just affect factories but trickles into everything from R&D spending to hiring plans.

The bond market has long been considered the best barometer of macro risk and it is quietly showing signs of stress. Treasury yields have risen not only because of sticky inflation and Fed policy, but because global investors are starting to ask tougher questions. Who will buy U.S. debt as deficits widen and debt service costs mount?

Foreign ownership of Treasuries is slipping, and in response, yields are creeping higher. This is a significant shift. For decades, U.S. debt has been the default safe haven during times of global stress. If that confidence erodes, everything from mortgage rates to the government’s ability to spend through a downturn could be affected.

And it’s not just America. Japan, another heavily indebted nation, is also facing rising yields. The yield on Japan’s 30-year JGB rose from 2.25% in April to 3.18% recently. This is a significant shift for a country that’s been anchored near zero rates for much of the past three decades. The global bond market appears to looking more at key debt ratios rather than central bank monetary policy.

While the S&P 500 may be back in the green for the year, it’s hardly impressive compared to some other markets. Germany’s DAX is up over 20%, Hong Kong’s Hang Seng has surged 18%, and even Mexico’s Bolsa is up 18%. The underperformance of U.S. equities, once the leader in global asset flows, suggests that capital is looking elsewhere for growth and value.

This divergence is happening just as American multinationals may begin to feel the sting of weakening global demand. In the second half of the year, we’re likely to see the delayed effects of lower international sales and softer branding power abroad. Consumers and governments alike are beginning to reassess their dependence on American firms—another trend with long-term consequences.

In this increasingly uncertain environment, where do investors go? Traditionally, the answer would be Treasuries or the U.S. dollar. But as trust in those pillars weakens, crypto is once again drawing attention, not just as a high-risk, high-reward tech play, but as a hedge against fiat instability.

Bitcoin is beginning to behave more like a macro asset. It rallied during U.S. banking scares in 2023, it found footing during global rate volatility, and now it stands as a possible beneficiary of the world’s pivot away from U.S. sovereign assets. Institutional interest continues to grow, driven in part by the rise of tokenized real-world assets and regulated digital infrastructure.

If capital continues to trickle out of U.S. bond markets, we would not be surprised to see more flows into Bitcoin, Ethereum, and the broader crypto ecosystem. These assets are not immune to volatility, but they increasingly represent a different kind of exposure—one that sits outside traditional debt and equity cycles.

The one outlier is the rise of AI which we are already seeing improve productivity and we think this is just getting started. Stronger global productivity will be good for equities and will offer as a much needed counterweight to the concerns around the US debt market.

And although the current markets appear to be showing signs of calm, we think investors should remain cautious.

Media of the Week: Signal for Bitcoin?

There are a lot of theories (maybe even conspiracies) about certain price actions in households items or cheap food products and the broader economy. For example, the Big Mac Index which was “was created by The Economist magazine as an informal way of measuring the purchasing power parity between different countries and currencies. The idea is that in every country, the Big Mac sold at McDonald’s is the same. The price of the Big Mac should reflect the local price of ingredients, wages and other expenses like advertising.”

One Twitter account mentions that the Snack Wrap is rumored to return in July and it could be a sign of a massive run for BTC. Now, a lot of this account’s tweets are just for fun but maybe he’s on to something. What do you think?