Crypto Grows Up

Gold, DeFi, and the Real World

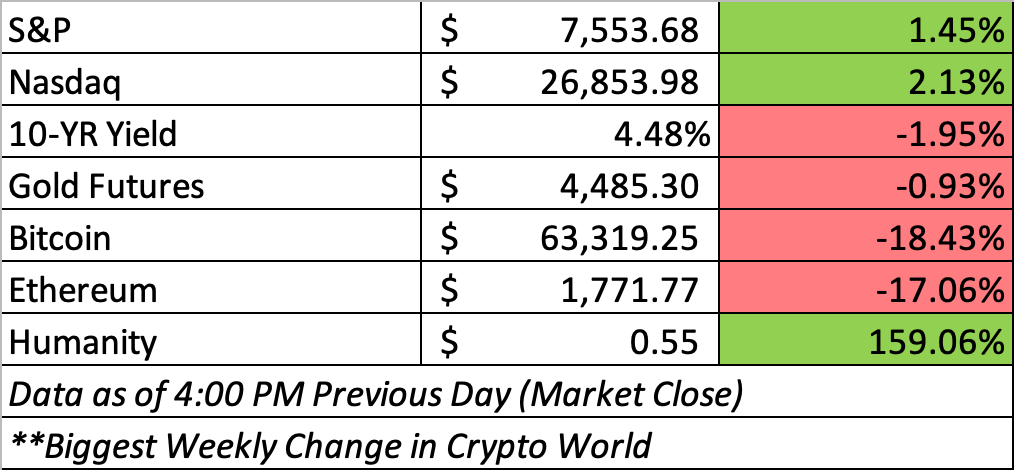

Good Morning. Stocks fell sharply on Wednesday as rising oil prices and Treasury yields sparked concerns that inflation could remain elevated due to escalating tensions between the U.S. and Iran. Overall, investors worried that stronger economic growth and rising energy costs could keep inflation elevated and make it harder for the Federal Reserve to lower interest rates.

Over the last week, crypto markets sold off as Bitcoin and Ethereum fell amid record ETF outflows, rising oil prices, and growing geopolitical and inflation concerns, pushing investors into a broader risk-off mood.

From spending gold with a Visa card to Hyperliquid’s rise as crypto’s breakout infrastructure story, this week’s newsletter explores how digital assets are moving from speculation to real-world utility. Check it out!

Crypto News You Can’t Miss: Tether Unveils New Product

Tether has partnered with digital banking firm Fasset to launch a Visa card that allows users to spend their holdings of Tether Gold (XAUT), a tokenized gold asset, anywhere Visa is accepted. The initiative aims to change the traditional role of gold from being primarily a store of value to a practical medium of exchange. When users make a purchase with the card, their XAUT is instantly converted into Tether’s U.S. dollar-backed stablecoin, USDT, and then into the local fiat currency needed to complete the transaction. According to Tether CEO Paolo Ardoino, the goal is to make tokenized gold more useful in everyday financial activities by integrating it seamlessly with existing payment systems.

The card also includes incentives designed to encourage users to hold and accumulate gold-backed assets. Eligible purchases can earn up to 6% cashback, which is paid in real time in XAUT, and a round-up feature automatically invests spare change from purchases back into XAUT. Each XAUT token represents one fine troy ounce of physical gold stored in Swiss vaults and independently audited. The token, which was first launched on Ethereum and later expanded to other networks such as BNB Chain, currently has a market capitalization of approximately $2.7 billion. The article also notes that although gold reached record highs earlier this year, both physical gold and XAUT were trading around $4,414 per ounce on Wednesday, roughly 20% below their annual peak. Overall, the new Visa card represents Tether’s effort to bridge traditional assets, stablecoins, and everyday payments by making tokenized gold easier to spend and invest in.

Has DeFi Finally Come of Age?

For much of the past decade, decentralized finance has been treated as both revolutionary and slightly impractical. It promised a financial system without gatekeepers, but too often delivered clunky interfaces, fragmented liquidity, slow execution and token incentives that looked more like promotional subsidies than durable business models. DeFi was exciting, but it did not always feel inevitable.

In just over three years, Hyperliquid has gone from an idea pursued by a small engineering-led team to one of the most valuable projects in crypto, with the HYPE token recently valued at more than $15 billion. That achievement matters not only because of the number itself, but because of how it was achieved. Hyperliquid was not built by a consortium of banks. It was not incubated by a major Wall Street exchange. It was not the result of a heavily funded venture-backed team spending hundreds of millions of dollars to buy market share. It was, at its core, a product of excellent engineering, sharp product judgment and disciplined execution.

The original problem Hyperliquid set out to solve was simple to describe and difficult to execute. Traders liked decentralized exchanges because they offered transparency and self-custody. They liked centralized exchanges because they were fast, liquid and easy to use. The conventional view was that users had to choose. If you wanted the speed of Binance or Coinbase, you accepted the risks of a centralized intermediary. If you wanted on-chain transparency, you accepted slower execution and a less professional trading experience.

Hyperliquid challenged that tradeoff. Rather than building another application on top of an existing general-purpose blockchain, the team built its own Layer 1 blockchain optimized for trading. Its core exchange infrastructure was designed to support an on-chain order book, fast settlement and a user experience that feels far closer to a centralized exchange than to the earlier generation of DeFi protocols. The result is not merely another decentralized exchange. It is an attempt to build exchange infrastructure natively on-chain.

That distinction is important. Much of early DeFi recreated familiar financial activities in a more open environment. Lending, borrowing, swapping and liquidity provision all moved on-chain, but the experience often remained niche. Hyperliquid suggests something more ambitious: that a blockchain-based venue can compete on performance, not just ideology. Users are not there only because they believe in decentralization. They are there because the product works.

The story is also striking because of what was absent. Hyperliquid did not emerge from the familiar crypto launch playbook of large venture allocations, aggressive marketing campaigns and insider token distributions. Its identity was built around a different set of principles: no outside investors, no paid market makers, no insider allocation and a large airdrop to actual users. In an industry often criticized for enriching insiders before communities, that was a meaningful statement. More importantly, it helped align the project’s narrative with its product. Hyperliquid was built for users first, and the token followed the usage.

This is where the “DeFi has come of age” argument becomes more serious. Mature financial infrastructure is not defined by slogans. It is defined by liquidity, reliability, revenue and trust. Hyperliquid now has all four in some measure. It has attracted deep trading activity. It has shown that on-chain order books can work at scale. It generates real fees. It has created a visible mechanism by which platform usage connects to token economics through buybacks and burns. For professional investors, that matters. The old criticism of crypto was that tokens had no relationship to cash flow or economic activity. Hyperliquid does not eliminate that debate, but it gives the market a much more concrete framework to analyze.

The broader implications are significant. If a small team of strong engineers can build a credible exchange venue in three years, then the next generation of financial infrastructure may not come exclusively from banks, brokers or exchanges. It may come from teams that understand both market structure and software architecture, and that are willing to rebuild the stack from first principles. This is the deeper lesson of Hyperliquid. DeFi is no longer only about replacing trust with code. It is about building better market infrastructure.

There are still risks. Hyperliquid operates in a regulatory environment that is evolving quickly. Perpetual futures are attracting the attention of U.S. regulators, and regulated competitors such as Coinbase and Kalshi may benefit from clearer access to American users. Hyperliquid also faces the usual challenges of crypto market cycles, token unlocks, validator decentralization and security. Coming of age does not mean becoming risk-free. It means becoming important enough that the risks are worth studying seriously.

That may be the most important shift. A few years ago, DeFi was easy for traditional finance to dismiss as experimental. Today, Hyperliquid shows that decentralized infrastructure can attract real users, generate real revenue and reach public-market scale with astonishing speed. It did not need a Wall Street pedigree to do it. It needed technical excellence, product focus and the ability to execute.

So has DeFi finally come of age? Not everywhere, and not all at once. But Hyperliquid is powerful evidence that the answer is beginning to be yes. The industry has moved beyond the question of whether on-chain finance can work in theory. The better question now is how much of global finance can eventually move onto infrastructure that is faster, more transparent and more open than the system it seeks to improve.

Media of the Week: Reserves vs. Backing

It is an important distinction and one worth highlighting. A reserve should be something highly liquid that can be used to meet redemptions quickly (cash, short-term Treasury bills, repo agreements, etc.). Backing assets can include less liquid things like real estate or longer-term loans that help ensure solvency but are not suitable for handling immediate withdrawals.